My girlfriend asked me to help her with her taxes this year because it was the first time she had a job paying any substantial wages. At the end of the year, she was curious how much she would get back as a refund, so I used one of the calculators online to come up with a refund estimate for her. However, when we did her taxes in February, we were delighted to find that she was getting a lot more back than we expected. This is because of something known as the Saver’s Credit.

The saver’s credit is something that a lot of new graduates may be able to take advantage of if they didn’t make a lot of money because they started a job mid-year. However, let me back up and say that you can’t be considered a full-time student for the tax filing year to take advantage of the tax savers credit. Below is how the IRS defines a full-time student:

Full-time student:

You are a full-time student if you are enrolled at a school for the number of hours or classes that the school considers full time. You must have been a full-time student for some part of each of 5 calendar months during the year. (The months need not be consecutive.)

My girlfriend wasn’t considered a full-time student in 2011 and was able to take advantage of the credit because her income was low in 2011. Although this could be a benefit to recent graduates, it is a great incentive for low to moderate income workers to save for retirement.

Eligibility for Tax Saver’s Credit

Here are some more details on the tax saver’s credit. To be eligible for the credit, your income limits must fall in the following ranges:

• Single, married filing separately, or qualifying widow(er), with income up to $27,750

• Head of Household with income up to $41,625

• Married Filing Jointly, with incomes up to $55,500

Additionally, to be eligible for the credit you have to be born before January 2, 1993, cannot have been a full-time student during the calendar year, and cannot be claimed as a dependent on another person’s return.

If you meet all of the criteria listed above and made contributions to a traditional or Roth IRA, 401k, 403b, and a variety of other retirement plans outlined on IRS form 8880, you can take advantage of the saver’s credit.

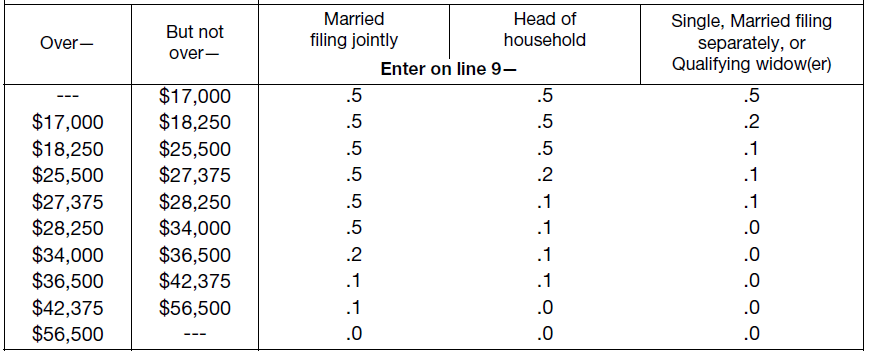

Below is a chart outlining the percentage of your qualifying contribution you can take as a credit on your 2011 taxes. Let’s look at a simple example of how this credit works.

The first two columns in the chart are based on adjusted gross income. The next three columns include the decimal to multiply your qualified contribution for the year. The maximum contribution eligible for the saver’s credit is $2,000, which means the maximum possible credit is $1,000 (.5 x $2,000 = $1,000).

Example:

Ann’s tax filing status is single. Also, Ann was not a full-time student and no one else claimed her as a dependent on their tax return. In 2011, Ann’s adjusted gross income was $25,000. Additionally, Ann contributed $2,000 to her 401k plan in 2011.

In this example, Ann meets the requirements to be eligible for the saver’s credit. Looking at the IRS chart, the multiplier for someone single with an adjusted gross income of$25,000 is is 0.1. Thus, Ann would would be eligible for a $200 saver’s credit.

This is definitely something to look into if your income was low in the year for whatever reason. However, you should always check with a tax professional to ensure that you are indeed eligible for the credit.

image credit:401K

Leave a Reply